OneUp Accounting: Overview Of Features For Small Business Bookkeeping

Bank reconciliation, integrations, and transaction matching in OneUp Accounting overview of small business bookkeeping

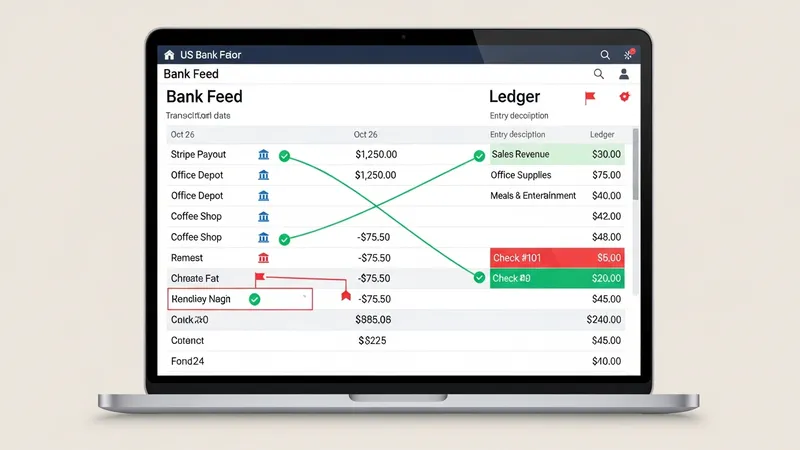

Bank reconciliation features in bookkeeping platforms typically import transactions from US banks through secure feeds or manual statement upload. Reconciliation workflows propose matches between imported transactions and recorded entries, and may flag mismatches such as uncleared checks or bank charges. For US small businesses, reconciling monthly or weekly is a common practice to maintain accurate cash balances and to detect errors or fraud. Reconciliation interfaces may also permit clearing of transfers between internal accounts and adjusting entries for fees or interest.

Integration with payment processors and merchant accounts helps reconcile deposits and fees. In the United States, merchant deposits may aggregate multiple sales into single bank deposits; a bookkeeping platform that records settlements and associated processing fees can simplify matching these aggregated amounts to individual invoices. Additionally, automatic import of bank feeds reduces manual CSV handling, though periodic review remains a typical control to ensure categorization rules remain aligned with account mappings.

Transaction matching rules often use vendor names, amounts, and dates to suggest reconciliations; these rules can be customized to reflect common vendor naming conventions in the US. For bookkeeping accuracy, it is common to maintain a chart of accounts structure that distinguishes operating expenses, cost of goods sold, payroll-related accounts, and tax liabilities. Properly mapped accounts support clearer reconciliation and more accurate period reporting when imported bank activity is assigned to the correct ledger categories.

When automated bank matching fails to resolve items, bookkeeping users typically perform manual reconciliation steps such as split transactions, recorded deposits in transit, or adjustment entries for bank fees. Keeping a documented reconciliation process and notes on adjustments can help when preparing materials for tax professionals or when responding to inquiries from US regulatory authorities. These practices may improve transparency of the bookkeeping records over time.